Table of Contents

Buy/Sell Your Unlisted Shares

Submit the details below to share a quote.

TL;DR

Coforge share price jumped about 11% after the company reported a strong Q4 FY 26, with net profit surging 134% YoY and revenue up 30% YoY. Underlying positives include a large executable order book, double digit revenue growth, and improving operating margins.

Introduction

Coforge share price surged Intraday after the IT service company posted a sharp improvement in its Q4 FY 26 performance. The net profit doubled and the revenue grew in high-teens to low thirties range, depending on the constant currency versus rupee view.

The 10%-11% rally on stocks reflected not just the earnings beat, but also renewed the optimism from domestic and global brokerages.

About Coforge

Coforge Limited registered itself as a public limited company on May 13, 1992. It was initially ‘NIIT Technologies Limited’. It is a global digital service and business solutions provider. They have in-depth domain expertise that specialise in industry verticals.

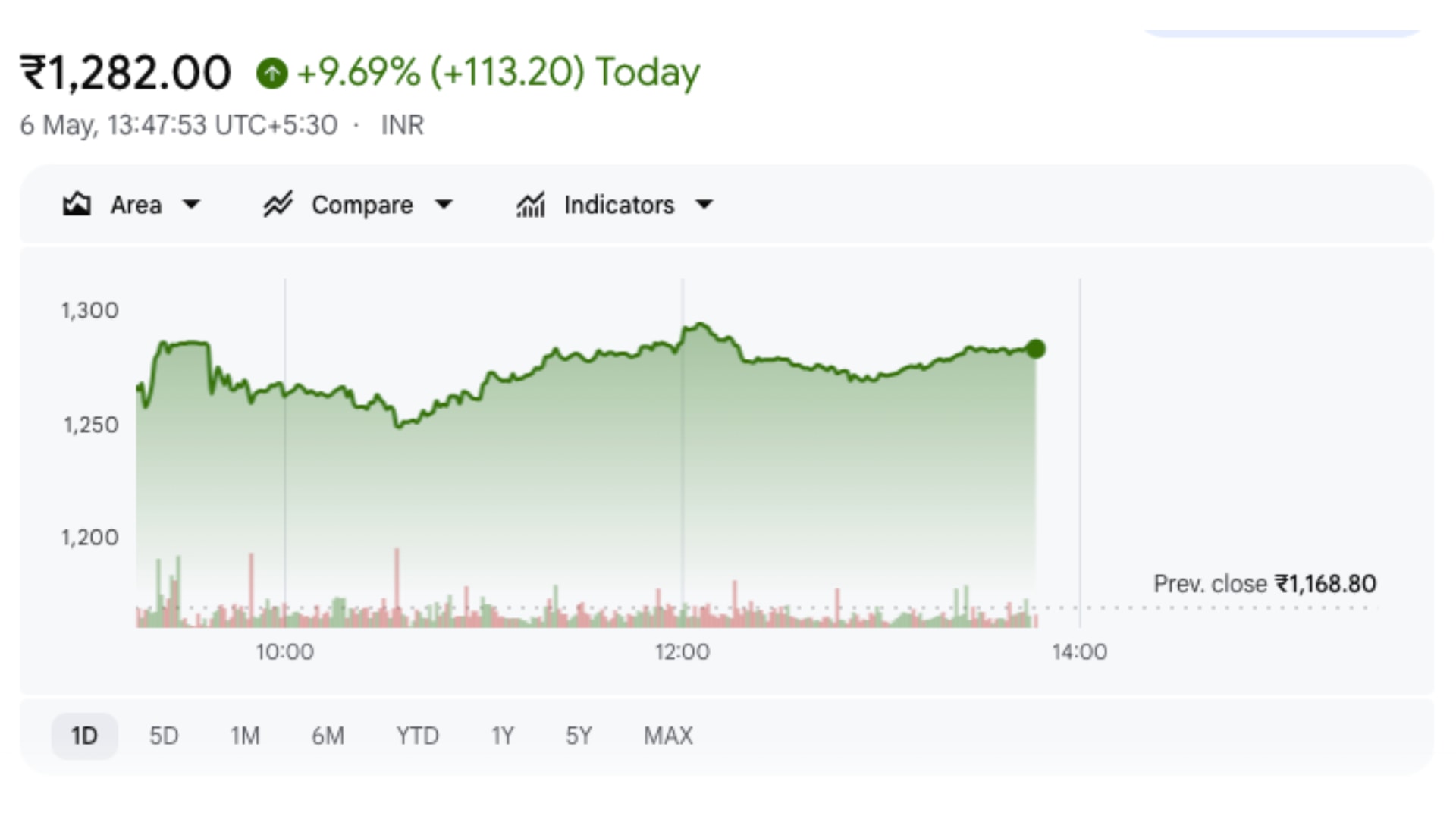

Coforge Share Price

Source: Google Finance

What Happened in Q4 FY 26 for Coforge?

The catalyst for the move of the Coforge share price was a robust Q4 earnings print. The company reported:

Net profit of about ₹612.3 crore, up 134% YoY and roughly 9% sequential growth which indicates both strong year-on-year improvement and steady progress across quarters.

Revenue in Q4 of around ₹4450.4 crore, a 30% You increase and roughly 5% sequential growth with constant currency revenue growth coming in at about 28.7% which suggests the numbers are not just currency-driven.

These figures combined with improving operating margins and a healthy order book pipeline are enough factors to spark a sharp intraday rally in Coforge share price to about ₹1,294, with

the stock rose around 10-11% on the day of the results.

Why Did Brokerages Turn Bullish?

Brokerages don’t upgrade based on the single quarter, instead they look at the trends, margins, and order-book quality. Here’s how Jefferies, Nomura, and Motilal Oswal have framed the Coforge Story.

Jefferies: Margin Strength and Cash Flows

Jefferies has set a target pricing around ₹1,860 on Coforge shortly after the Q4 results. The firm highlighted that:

As EBIT margins got better to 13.4% in Q4, which is 1.2% higher sequentially, and it remained above 13% in the last four quarters.

Also the free cash-flow conversion was stronger. The operating cash flow at ₹1,949 crore for FY 26, about 1.4x of reported net profit, indicates healthier working capital and collection. (Source: ET)

These factors suggest that Coforge’s growth is increasingly profitable and cash-generating. It supports the valuation that Jefferies sees in Coforge share price.

Nomura: Top Mid Cap IT Pick

Nomura had identified Coforge as a top-mid cap IT bet and assigned a Buy rating with a ₹2,000 target, even before the Q4 rallies. The firm appreciated:

Strong execution in the last 12-18 months, with revenue growth accelerating and margins holding up.

The placement of the company in the modern digital and cloud services and this tends to fetch higher valuations that legacy IT plays. (Source: Business Standard)

Nomura call implies that Coforge has crossed that threshold, which is why the brokerage sees significant room for Coforge share price appreciation.

Motilal Oswal: AI-led Demand and Deal Momentum

Motilal Oswal has also stayed bullish, with multiple reports talking up to 54% upside in Coforge and in prior notes, even higher end targets. Key points the firm stresses:

Strong demand for AI driven solutions, automation, and cloud modernisation, and all of these are visible in Coforge’s deal pipeline.

Resilience in maintenance and security-led integration work, which forms the stable base of the recurring revenue.

When combined with Coforge’s FY 26 revenue growth of roughly 36% YoY and margin expansion to 14.4% EBIT, Motilal Oswal can justify the upside projections on Coforge share price. (Source: BS)

What “Up to 80% Upside” Really Means?

Some analysts think that the normal Coforge’s share price could rise a lot from its current level. It is the best-case estimate for the share price to go high, but is not a guarantee. It is basically a hopeful target, based on things like strong earnings, good business growth, and future demand.

If the company keeps performing well, the stock can move towards that target. But on the contrary if the business slows down, margins shrink, or the market turns weak, the stock may not reach that level. (Source: Business Standard)

Risks to the Coforge Share Price Story

Even with a strong Q4 and optimistic broker views, the Coforge shares carry a risk.This is what investors must observe:

IT spending cycles: Global clients may gradually slow down the discretionary digital projects, in case the macro conditions weaken. This can further stress new-deal wins and future growth.

Margin Pressure: If wage inflation, travel costs, and value added staffing work rise, Coforge’s EBIT margin could stabilise.

Execution Risk: The order book in the pipeline is a good thing but if it slips, the confidence in the stock can erode fast.

Conclusion

Coforge share price moved up and has yielded stronger returns of close to 1,201.56 percent in the last 10 years. The company posted a strong Q4 FY 26, with profit surging and revenue growing robustly. While the fundamentals today look better, investors should treat this as a range of expectations, and not a forecast.

FAQs

Why did Coforge share price jump after Q4?

Coforge share price increased after the impressive Q4 FY 26. The net profit rose about 134% YoY.

Is Coforge fundamentally a strong company now?

Yes, Coforge looks stronger on paper with its FY 26 revenue of about ₹16,420 crore which is 35.9% YoY.

What is the current share price of Coforge?

The current share price of Coforge is ₹1,217.

You may also like to read

What Are The Different Classes Of Shares Issued In India?

Different Classes of Assets In The Financial Market

Follow These Simple Share Market Tips While Investing

Importance of Investing in Unlisted Shares

Step-by-step Process Of Transferring Unlisted Shares (Off-market)

Pre IPO Success Stories To Start Your Unlisted Share Trading

What Is The Expected Return Of Unlisted Shares?

A Detailed Guide On How To Buy Unlisted Shares In India

Know Your Tax Implications Before Investing In Unlisted Shares

Common Mistakes To Avoid While Investing In Unlisted Shares

How To Pick Best Performing Unlisted Stocks in India?

Risks And Rewards Associated With Unlisted Share Investment

Difference Between Start-Up Investing And Unlisted Shares?

IPO Process in India: Key Steps Explained Clearly

Revealed: The Real Picture of Unlisted Shares in Grey Market

Key Financial Ratios And How To Use Them To Analyse Your Investment

101 Guide For Beginners: What Is Pre IPO Share Market?

10 Golden Rules Of Investing In Stock Market

Listed Shares Vs. Unlisted Shares - Detailed Comparison

The Dark Side of Paytm's IPO Explained In Details

What Leads to Delisting of Shares and What Goes Behind The Scenes?

When Should You Review Your Portfolio Professionally?

In-Depth Analysis of Pre-IPO Shares for Portfolio Growth

PharmEasy Unlisted Price Falls 70%. Here's why

Delaying Pre-IPO Investments? Here’s What You Risk

An NRI’s Guide To Invest In Unlisted Shares In India

Guide To Filter The Most Profitable Unlisted Companies In India

A Comprehensive Guide On Follow-on Stocks

Care Health Insurance

Smart Strategy to Buy & Sell Unlisted Shares Professionally

Top Highly Profitable Unlisted Companies In India To Look For As An Investor

Upcoming IPOs In 2022-2023

Expert’s Driven Roadmap To Research A Startup IPO

Capgemini Unlisted Shares: Is The Risk Worth?

HDFC Sec vs HDB Financial: Which Is the Better Pick?

Detailed Guide To Calculate Capital Gains on Unlisted Shares

Dematerialisation of Unlisted Shares and Its Impact On Shareholders

How are B9 Beverages Pvt Ltd (Bira91) Unlisted Shares Gaining Pace Again?

Reliance Retail: The Success Story of India's Largest Retail Brand

The Future Of Unlisted Shares In the Fintech Market

Employee Stock Ownership Plan: What, How, and Why?

Studds Unlisted Shares: 6 Reasons to Buy Now

LAVA’s Unlisted Shares Soar Under Atmanirbhar Push

NSE vs BSE: Detailed 101 Market Share Comparison

The Role Of Corporate Governance And Management In Unlisted Companies

What's Temperature Ahead Of Tata Technologies' ₹4,000 Cr. IPO?

The Future Outlook For Unlisted Shares As An Investment Option

How to Buy and Sell Unlisted Shares in India?

The Benefits And Drawbacks Of Investing In Unlisted Shares