The Central Electricity Regulatory Commission (CERC) is bringing a new trading framework which could impact the operations of power exchanges like IEX, PXIL and HPX. The regulator has approved pre-specified time slots for power trading, rejecting the demand for customized trading slots on power exchanges.

Grid India vs Utilities Face Off On Trading Flexibility

Several utilities and market participants like BSES Rajdhani, BSES Yamuna, Rajasthan Urja Vikas and UPPCL sought flexibility from the CERC through region-wise peak-hour contracts, seasonal peak definitions and customised two-hour delivery slots. The reason they gave was that different state-level demands called for more flexible contract structures.

But Grid India opposed the region-specific peak hours contracts, stating that peak demand timings vary significantly across regions and months. If every state began creating their own customer contract, trading liquidity would be divided into too many segments, especially in the Term Ahead Market.

CERC agreed with Grid India that price volatility and spikes in India are mainly caused by the difference between

daytime (when solar is available) and

nighttime/non-solar hours (when solar disappears)

Not due to the individual state-wise demand differences. That’s why CERC-approved solar and non-solar hours at the national level compared to the regional level.

CERC Protecting Liquidity And Price Discovery

Earlier, power exchanges such as Indian Energy Exchange Limited (IEX), Power Exchange India Limited (PXIL), and Hindustan Power Exchange Limited (HPX) allowed buyers and sellers to create specific hourly or customised exchange contracts. For example, a utility could buy power for only a 2-hour slot in a specific region.

But now CERC has stopped this flexible system.

The CERC said in a detailed order dated 21st May 2026, covering the petitions filed by Indian Energy Exchange Limited (IEX), Power Exchange India Limited (PXIL) and Hindustan Power Exchange Limited (HPX), where the regulator was of the view that too many customised contracts would split trading activity into smaller pieces.

CERC is of the view that:

If everyone traded different products at different times, liquidity would be fragmented.

Fewer buyers and sellers in each contract can weaken price discovery.

Power pricing will become volatile and inefficient.

By passing this order, CERC wants more buyers and sellers in the same contract, which can lead to better liquidity and strong benchmark pricing.

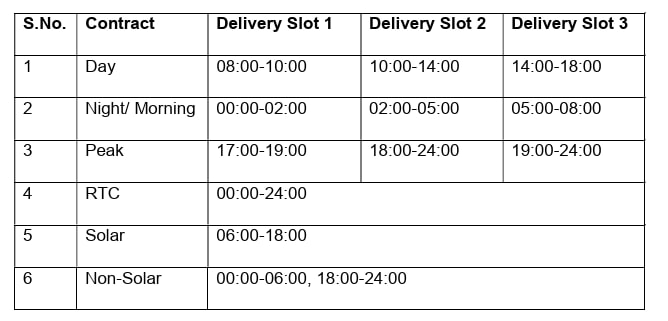

CERC’s Pre-Approved Time Slots

The commission, aligned with the recommendation of the Grid Controller of India, approved a national-level slot structure based on solar and non-solar hours. Under the new framework, here is how the slots will work:

Source: CERC Order

This order has come after CERC earlier released a directive on 28th April 2025, asking power exchanges to stop user-defined time slots, including hourly slots, in TAM, G-TAM and HP-TAM contracts.

Impact On IEX Dominance, PXIL And HPX Under Standardised Vs Fragmented Contract Rules

Fragment contract rules generally tend to favour the exchanges with the largest volume. On the other hand, standardised rules make the market easier to compare and compete. Here are the possible effects on the 3 exchanges:

For IEX

IEX dominates the power exchange trading market due to its liquidity and effective price discovery venue. The fragment contract rules make the exchange with the deepest liquidity pool naturally more attractive for trading flow. Thus, IEX has been dominating this market.

Standardising contract rules can weaken its moat, making contracts uniform across exchanges. This can lead to slower growth, some market share leakage and pressure on margins for IEX.

For PXIL and HPX

In flexible contracts, PXIL and HPX have been structurally disadvantaged as compared to IEX. Here, PXIL and HPX need to depend on product differentiation that may not be able to overcome IEX’s liquidity advantage.

Power Exchange India Unlisted Shares and Hindustan Power Exchange Limited Unlisted Shares can benefit from standard contracts because the entry barrier for liquidity-sensitive users will be lower now. These 2 exchanges no longer need to invent customer slots or rely on niche products to attract trading flow