1.jpg)

Mohan Meakin, one of India’s oldest liquor companies, known for its legacy alcohol brands and premium spirits portfolio, reported a strong FY26 performance, with Mohan Meakin profit jumping over 52% despite only moderate revenue growth.

In this blog, we will analyse Mohan Meakin results for FY26, including Mohan Meakin profit growth, margin expansion, balance sheet strength, and the company’s long-term growth potential ahead.

Mohan Meakin Financial Analysis

Particulars (in Rs. Cr) | FY26 | FY25 | YoY Change |

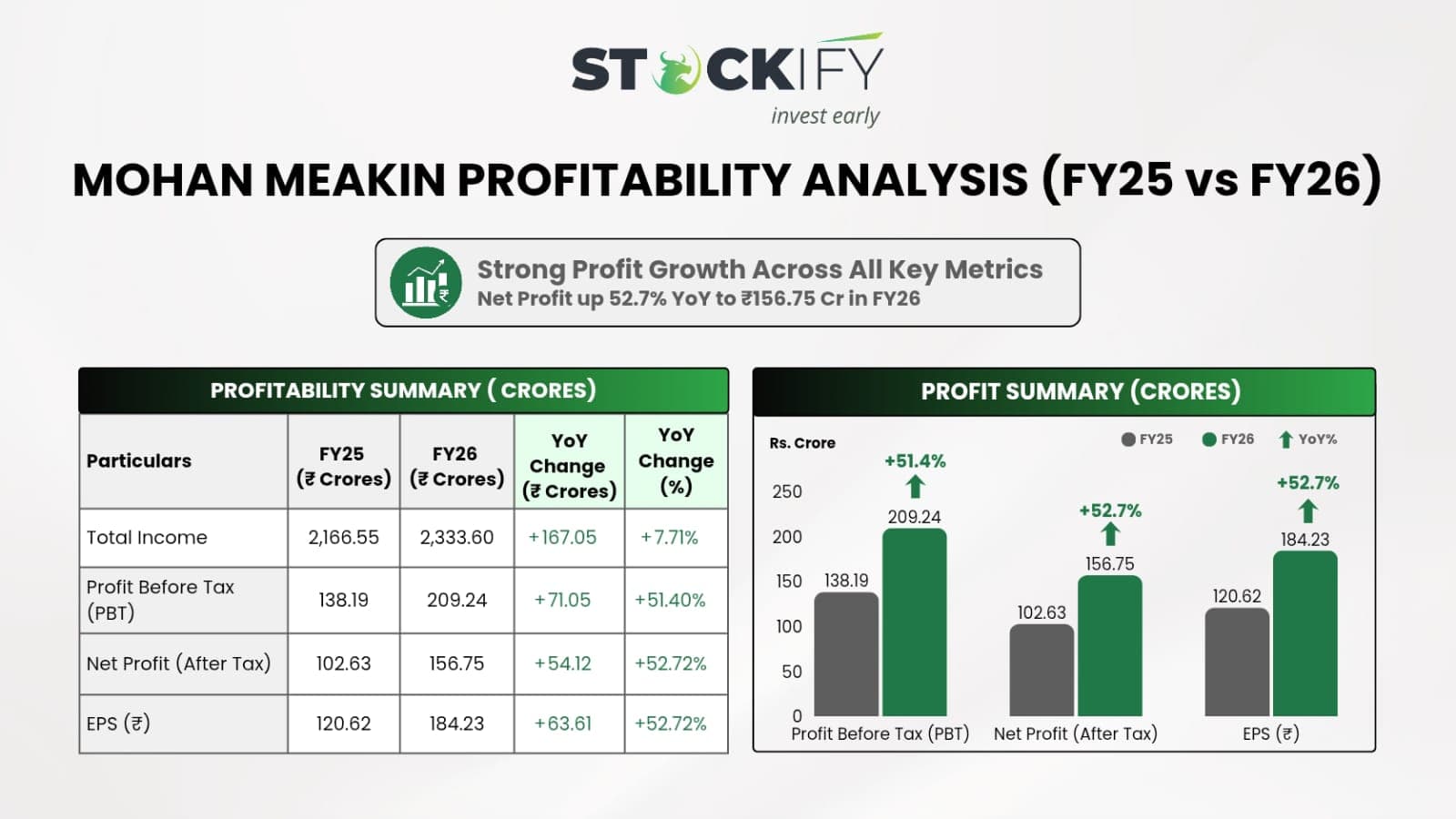

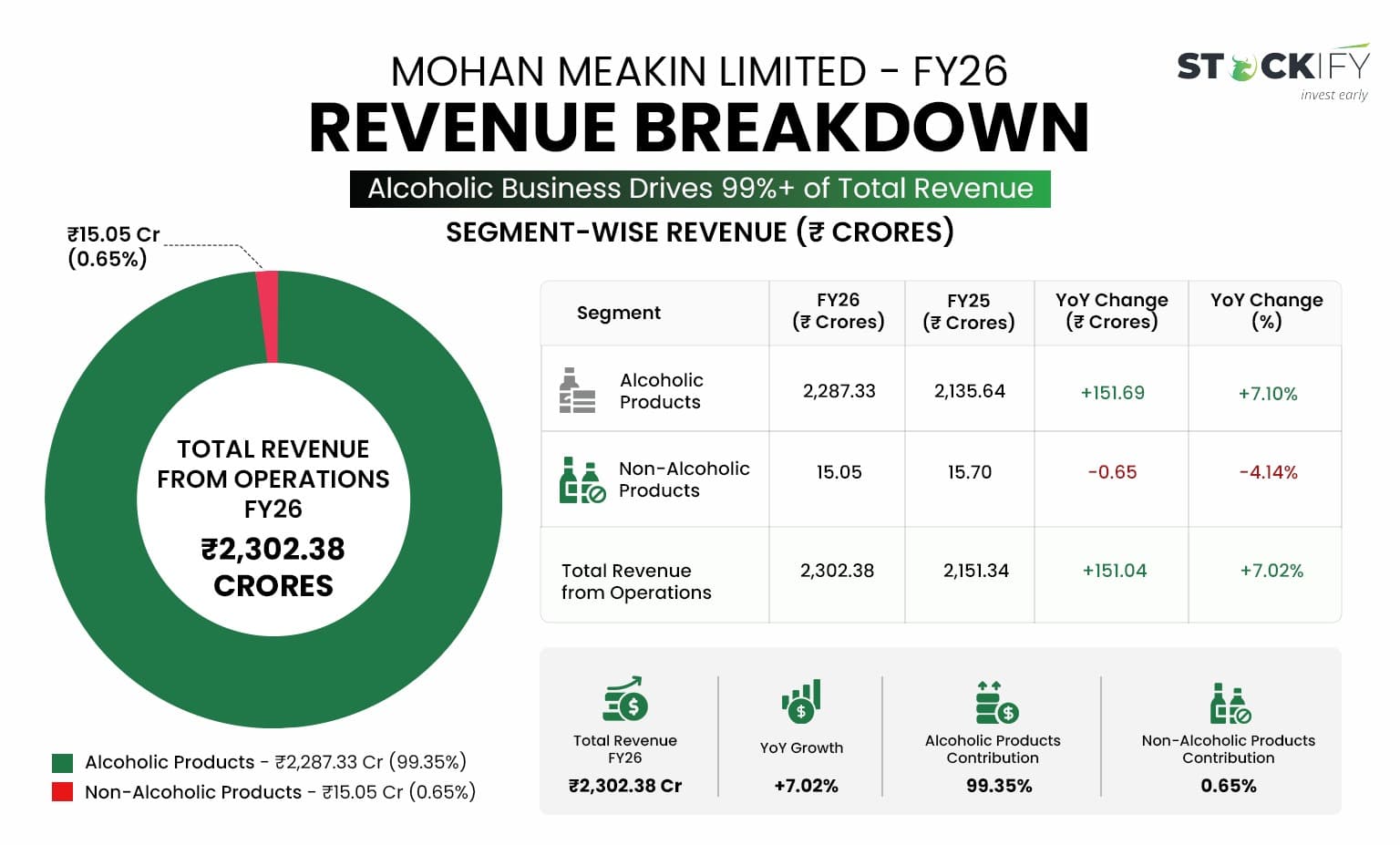

Revenue from Operations | 2,302.38 | 2,151.34 | +7.2% |

Total Income | 2,333.60 | 2,166.55 | +7.7% |

Profit Before Tax (PBT) | 209.24 | 138.19 | +51.4% |

EBITDA | 220.55 | 148.81 | +48.2% |

EBITDA Margin | 9.6% | 6.9% | |

Net Profit | 156.75 | 102.63 | +52.7% |

EPS | 184.23 | 120.62 | +52.7% |

Source: Mohan Meakin Financials

A. Revenue Was Stable, But Profits Stole The Show

Mohan Meakin Revenue jumped to roughly 7% annually, which is Rs.2,302.38 cr in FY26, compared to Rs.2,151.34 cr in FY25.

However, profitability improved much faster than revenue. The company’s profit before tax rose sharply to Rs.209.24 cr, while net profit jumped to Rs.156.75 cr. This means that Mohan Meakin Profit grew over 50%, far ahead of revenue growth.

Why Did PAT Grow Faster Than Revenue?

1. Margin Expansion

The company significantly improved its profitability margins (PBT) from 6.4% to 9.0% during FY26. Whereas PAT Margin improved from 4.7% to 6.7%. This means the company earned more profit from every rupee of revenue.

2. Better Product Mix & Realisations

Higher contributions from premium alcoholic products likely improved pricing power, average selling prices, and overall profitability during FY26. Since premium products generally carry higher margins than mass-market offerings, they supported stronger earnings growth for the company.

3. Controlled Expense Growth

While revenue increased in FY26, expenses grew at a slower pace, helping operating leverage improve. As a result, incremental sales translated into disproportionately higher profits, supported by controlled employee costs, finance expenses, and operational overheads.

4. Improved Working Capital Efficiency

Trade receivables reduced from Rs. 112.15 Cr to Rs. 82.28 Cr. Here, the company improved cash conversion and collections. This supports stronger profitability quality.

5. Low Debt Burden Helped Net Profit

The company operates with very low borrowings at Rs 4.29 Cr in FY26. Therefore, lower interest costs improved PAT conversion, and a strong balance sheet reduced financial pressure.

B. Margins Expanded Significantly in FY26

The major positive in Mohan Meakin's results in FY26 was margin expansion. The company improved its EBITDA margin from 6.9% to 9.6%, while PBT margin increased from 6.4% to 9.0% and PAT margin improved from 4.7% to 6.7%. That is a substantial improvement for a consumer alcohol business and suggests improved cost efficiency and healthier operating leverage.

C. Core Alcohol Operations Continue to Dominate Revenue

Segment Revenue Breakdown

The alcoholic beverages division contributes almost the entire revenue base of the company, making it the core driver behind most Mohan Meakin products. The company’s portfolio includes premium rum, whisky, brandy, vodka, gin, and beer brands, while its non-alcoholic business remains comparatively very small.

D. Expenses Grew Slowly Compared to Profit

Expense Head (in Rs. Cr) | FY26 |

Cost of Materials Consumed | 260.06 |

Purchase of Stock-in-Trade | 1,493.13 |

Employee Benefits Expense | 61.32 |

Other Expenses | 163.14 |

The slower pace of expense growth helped improve profitability and margins. Hence, the company appears to have benefited from better inventory management and stronger cost control.

E. Mohan Meakin Net Worth Strengthened Significantly

Particulars (in Rs. Cr) | FY26 | FY25 |

Mohan Meakin Net Worth / Equity | 621.63 | 470.18 |

Total Assets | 813.95 | 651.91 |

Borrowings | 4.29 | 4.29 |

Return on Equity (ROE) | 28.7% | 21.8% |

Debt-to-Equity Ratio | 0.01x | 0.01x |

Operating Cash Flow Growth | 73.8% |

Mohan Meakin net worth increased to Rs.621.63 Cr, and total assets increased to Rs.813.95 Cr. Despite business expansion, borrowings remained extremely low at Rs 4.29 Cr, reflecting strong balance sheet quality and low financial risk.

The company’s ROE increased by nearly 7%, reflecting improved earnings efficiency and better returns for shareholders. Meanwhile, debt remained almost negligible at 0.01x, highlighting a very strong balance sheet with minimal financial risk.

Additionally, operating cash flow growth surged 73.8% during FY26, indicating that profit growth was supported by actual cash generation rather than only accounting gains. This also reflects improving working capital efficiency and stronger operational quality.

Can Mohan Meakin Give Significant Growth Ahead?

Mohan Meakin possibly delivers significant growth in the future as

Strong Profit Growth and margins expensed sharply in FY26

Here business efficiency and profitability improved.

Low Debt Provides Expansion Flexibility

Borrowings remained extremely low at just Rs 4.29 Cr, which could help in future investments and capacity expansion.

Operating Cash Flow Improved Strongly

Operating cash flow jumped 73.8% to Rs 167.79 Cr, indicating healthier earnings quality and stronger cash generation.

Revenue Growth Still Moderate

Revenue grew only 7.02% in FY26. It reflects that Mohan Meakin profit growth could be largely driven by efficiency and margin expansion.

Premiumisation Could Support Growth

Alcoholic products contributed over 99% of total revenue. This means that the rising demand for premium liquor products could improve realisations and margins further.

Overall, Mohan Meakin could appear capable of delivering steady and profitable growth, but sustained long-term expansion will likely depend on stronger revenue acceleration, premium product growth, and continued margin improvement. Thus, Mohan Meakin Limited Unlisted Shares can attract major eyeballs from investors, especially when the company files its DRHP for an IPO.

.jpeg)